Selan Update 2023

Selan Update 2023

"Wait long enough, and people will surprise and impress you." Randy Pausch

I did not expect to write an update on the business so soon. I figured the management would need a few more quarters to settle down but I am always ready to be surprised.

Selan came out with results and its second investor presentation with a few more crumbs to follow on future business strategy:

a) Ekeing out operational efficiencies

i) Sweating existing assets:

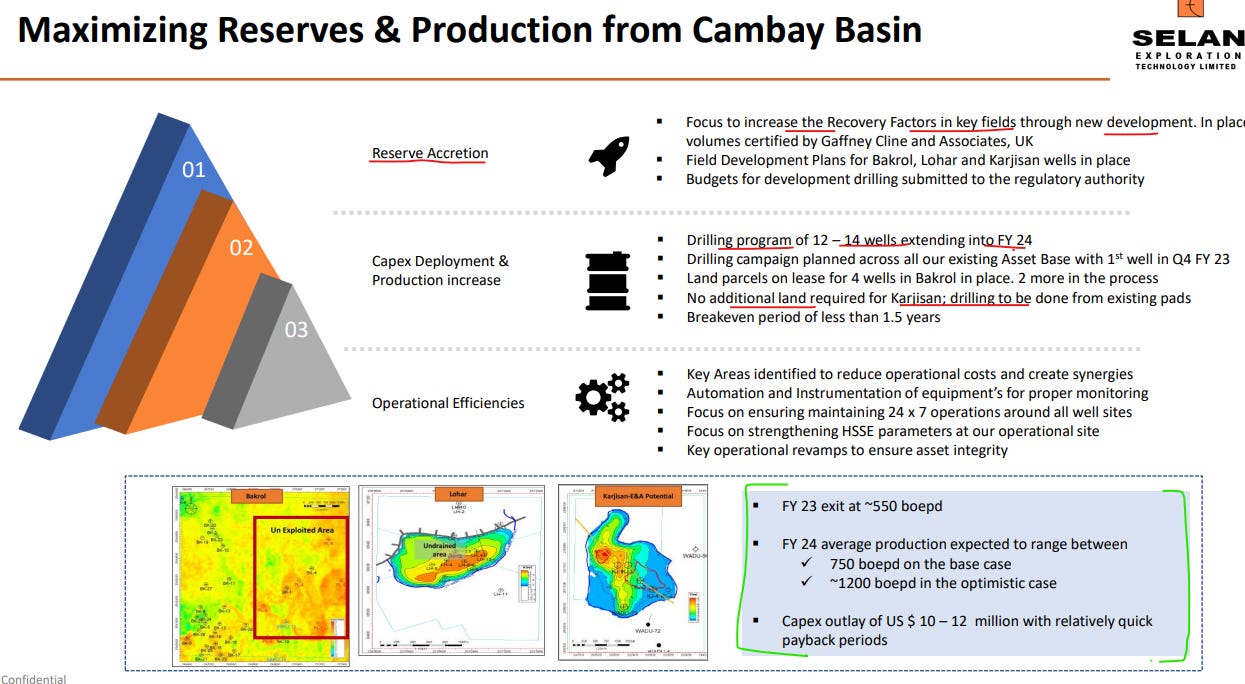

The management has indicated to sweat the existing assets by increasing drilling from existing Bakrol fields. Lohar and Karjisan assets were low-hanging fruits and management seems to shift its focus as well.

The management also has given its first-ever guidance to exit FY 23 exit at 550 Boped* while in Q3 the management achieved c.a. 500 Boped (see calculation below) so the exit run rate seems rather possible.

Further, management aims to achieve 750 boepd (in a base case) and 1,200 boepd (optimistic). Per my math, if they end up even achieving 750 boepd they will be at a revenue run rate of 190 crores with 45-50% EBITDA margins which work out to 85-90 crores. While the stock still trades at a measly market cap of 330 crores with 220 crores cash on the balance sheet resulting in an EV of 141 crores!

ii) Cost synergies: the presentation talks about reducing operational costs and achieving synergies. Although, one might observe that other expenses have increased it could be on account of expenses on filing tenders (will have to find out more). I would give them the benefit of doubt for this one.

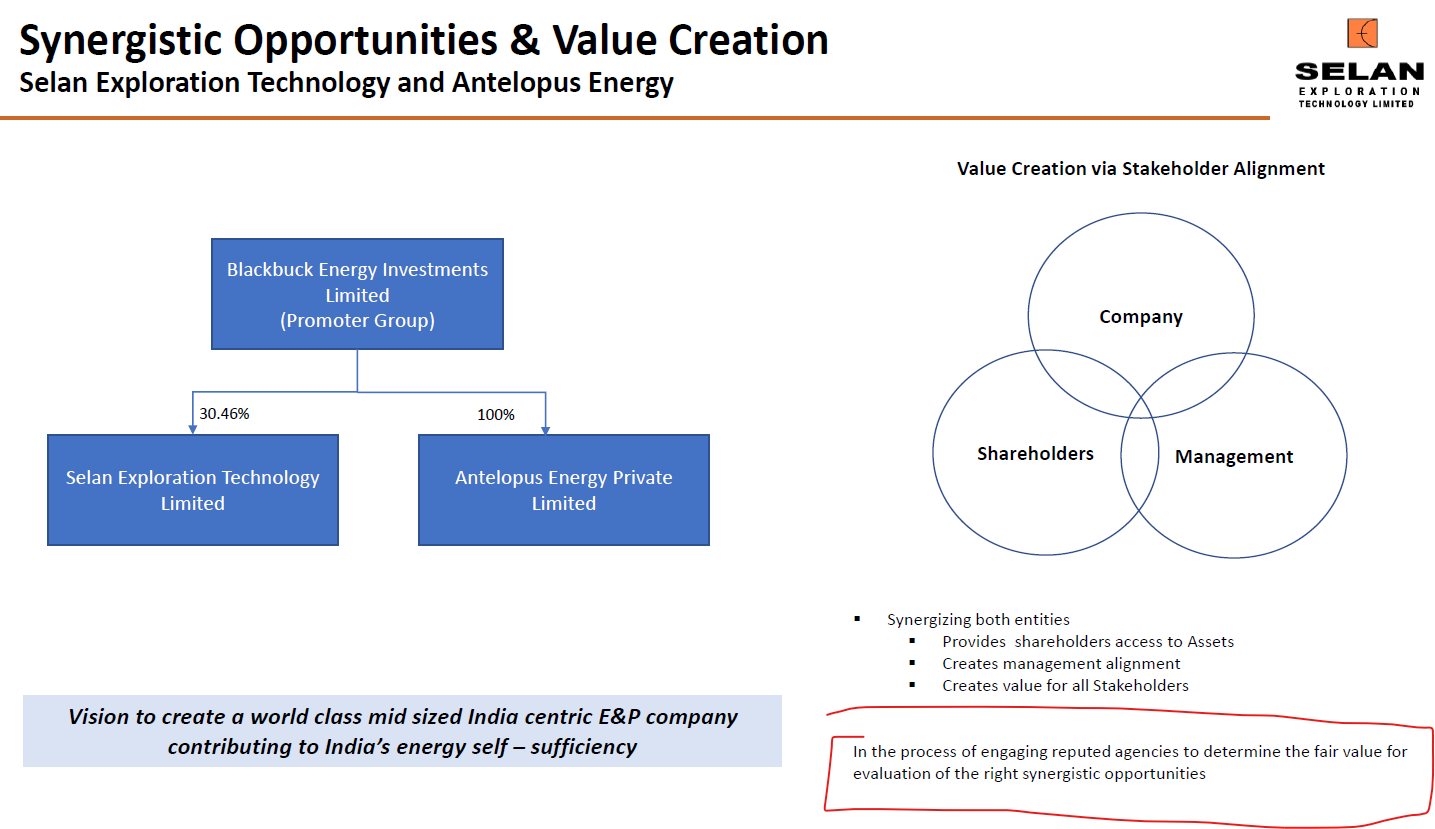

b) The merger:

the management has announced its plans for merging Antelopus with Selan to create a larger entity focusing on E&P-centric activities. Something we anticipated and are glad that the timeline was sooner than later setting aside the uncertainty.

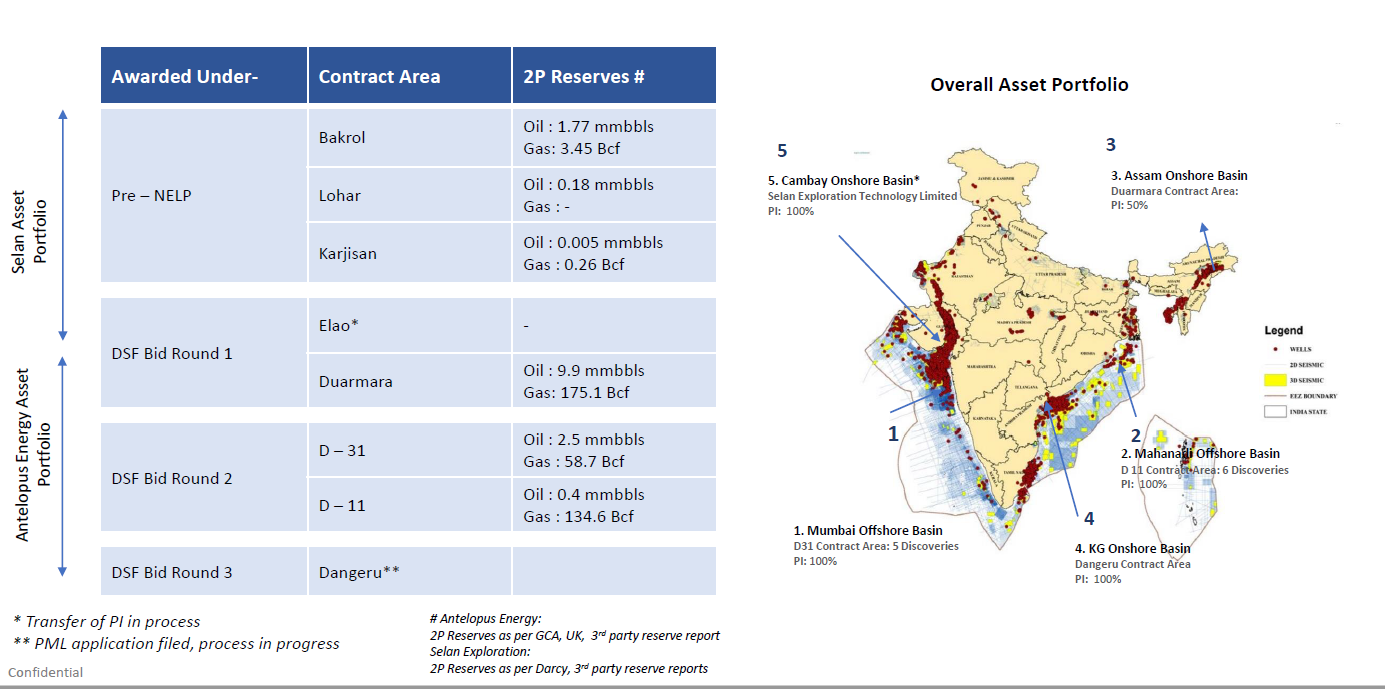

Selan’s financial resources will be useful to monetize Antelopus energy’s assets and bid for the DSF rounds.

Key question markets will wait and watch is the merger valuation ratio and the timeline before rerating the stock. This merger ratio will also set a precedent for how management intends to treat its minority shareholders.

c) Operational numbers:

Backing out the operational numbers by taking an average crude rate and exchange rate. I estimate that the business exited Q3’23 slightly below 500 boepd if I simulate the 750 barrels (with average crude and fx nos) I arrive at an operational revenue of 190 crores.

One can argue re the volatility of oil price and forex rates and can flex their assumptions around the same.

*Boped: Barrels of oil equivalent per day

Please note the number of barrels is an approximation since the business also has some natural gas sales but since they do not break it out in quarterly numbers it’s hard to model the same. I estimate that it’s not a large number so as to materially influence the results.

Margin of Safety is a pre-prerequisite for me and I feel positive about current developments in the business but continue to monitor execution and M&A progress.

Note: My family and clients have a long position in the business mentioned above. The above does not constitute any solicitation to invest.

Yep it was one of the members from the team. Still figuring out the space and it’s competitors. Looks quite interesting from future prospects.

How does this look to you ;-)

https://www.moneycontrol.com/news/india/govt-taking-strenuous-steps-to-scale-up-oil-exploration-production-oil-minister-puri-10031351.html