A small cap with a potential to turnaround

A small cap with a potential to turnaround

Selan Explorations Technology Ltd has often been discussed as a value trap but a change is afoot which might lead to rerating in the name.

“It’s not what you buy that determines your results, it’s what you pay for it. And what you pay – the security’s price and its relationship to intrinsic value – is determined by investor psychology and the resulting behavior” Mastering the market cycle, Howard Marks

What do you get when a nano-cap oil and gas business trades less than 3x EV/EBIT, led by a seasoned management team and backed by one of the smartest capital allocators? A lollapalooza!

Table of Contents

a) Executive Summary

b) Background

c) Management

d) Industry

e) Catalyst

f) Financials

g) Valuations

a) Executive Summary

Selan Explorations Technology Ltd ("the Company" or "Selan") is an Indian micro-cap (market capitalization of c.a. 265 crores) with hefty cash on the books of c.a. 200 crores resulting in an EV of 65 crores. The business generated an EBITDA of c.a. 34 crores (includes interest income of 7 crores) in 2022. This implies that the company trades at an EV/EBITDA of about 2x TTM or 3x TTM (ex-other income).

The Company faced multiple setbacks over the last decade combined with the inability to ramp production which has led to disappointed shareholders. Recently, a new management team (backed by some of the best global capital allocators) bought out the majority stake of the promoter which led to an open offer. The new promoters own 30% of the business and have brought in an industry stalwart to eke out more efficiency in the business.

My hypothesis is that Selan’s acquisition has been done to gain access to the cash on the Company’s balance sheet and use it to build Antelopus’s India’s business (another O&G venture backed by new promoters). In order to access the cash, the promoters will most likely reverse merge Antelopus India into Selan and unlock value.

Key risks would be a) new management misallocates cash. b) existing 2P reserves at Selan are far lower than estimated. c) new projects might take far longer to commercialize and scale.

The new promoter entity is backed by seasoned capital allocators so I would regard misallocation of cash as a low probability event. The new CEO, Suniti Bhat, has spent some time at Cairn and has a great operational track record to estimate these reserves. Further, his incentive structure is also aligned so if the Company does well he will do well. Therefore, I assume the severity of this risk to be low. While business projects getting delayed is a serious business risk and one would need to closely monitor this. There have been instances of projects getting delayed for environmental approval or other delays.

The bottom line is that you are buying a business (now trading below its open offer price) where you get your capital back in less than 3 years with multiple upside optionalities and while you are at it you get a rock star team working on your behalf for a pittance!

Naphtha, an ancient Persian word for a dark liquid coming from the ground, was adopted in classical Greek but most European languages eventually accepted variations of the Greek rock oil, pesqe’kaio – English petroleum, French pétrole, Italian petrolio – or its literal translations, such as German Erdöl, Dutch aardolie Oil, Vaclav Smil

b) Background

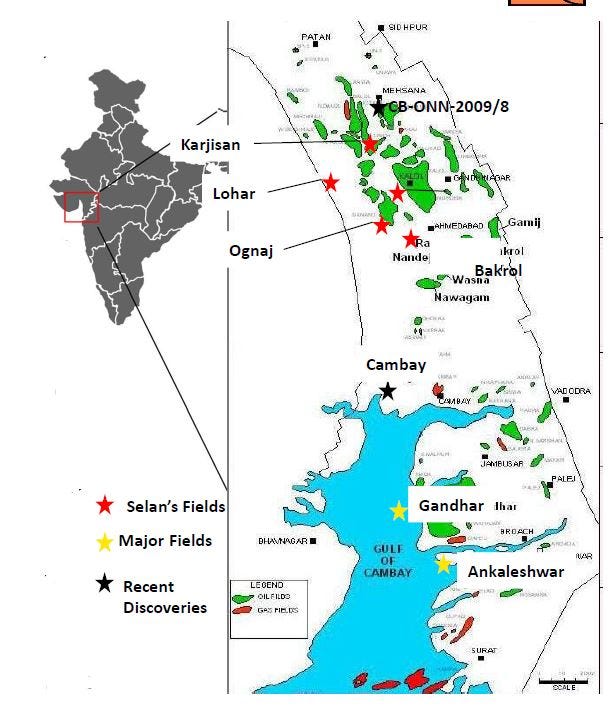

Selan Oil Exploration Technology is engaged in Oil and gas exploration projects and operates across four oil fields in Cambay Basin, Gujarat.

Source: Management Presentation May 2020

Cambay Basin

In 1958, ONGC drilled its first exploratory well on Lunej structure near Cambay. This turned out to be a discovery well, which produced oil and gas. The discovery of oil in Ankleshwar structure in 1960 gave boost to the exploration in the Cambay Basin. Over 2,318 exploratory wells have been drilled in Cambay Basin.

The Government of India and the Company signed Production Sharing Contracts (PSCs) in 1995 for Bakrol, Indrora and Lohar Oilfields.

Bakrol

Bakrol oil and gas field is located in the onshore Cambay Basin. Bakrol is a small onshore field with an area of 36 Sq.kms.

The field was discovered by ONGC in 1966. ONGC drilled 7 wells for the exploration and exploitation of Kalol pay zones viz. The field was put on production during which ONGC had produced 35,064 barrels of oil.

The oil field was awarded to the Company under Pre NELP round and a Production Sharing Contract (PSC) was signed between Govt. of India (GoI) and the Company in March 1995. The Company retains 100% economic ownership of the fields and pays royalty to the government.

Selan has been developing this field since 1995 including acquisition and interpretation of 2-D and 3-D seismic data and drilling of 22 wells.

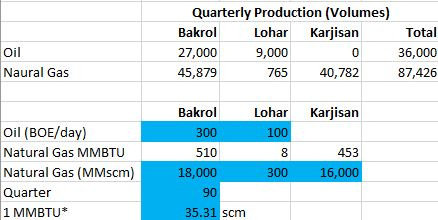

As of March 2021, there are 23 producing wells in the Bakrol. Bakrol produces 300 barrels and 18,000 SCM of oil and gas per day. Bakrol has produced c.a. 2.67 million barrels of crude oil and 112 MMscm of associated natural gas since these fields were taken over from ONGC.

Lohar

Lohar oil and gas field is located in the onshore Cambay Basin in Mehsana District of Gujarat State, India. Lohar is a small-sized discovered onshore field with an area of 5 sq km.

The field was discovered by ONGC in 1981. ONGC drilled 3 wells for the exploration and exploitation of Kalol pay zones K-III & IV out of which 1 well as oil/gas bearing. The field was under production by OMGC and produced 10,871 barrels of oil.

Similar to Bakrol the Company entered into a PSCin March 1995 retaining 100% ownership.

Selan has developed this field since 1995 including acquisition and interpretation of 2-D & 3-D seismic data (process data obtained from ONGC) and drilling of 10 wells. The additional data and interpretations estimate the discovered Oil In-Place (IOIP) is 3.49 MMstb.

As of March 2021, there are 6 producing wells in the Lohar produces is c.a. 100 barrels and 300 SCM of oil and gas per day respectively. Lohar has produced nearly 0.84 million barrels of crude oil and 2.02 MMscm of associated natural gas cumulatively post take over in October 1995.

Karjisan

Karjisan oil and gas field is located in the onshore Cambay basin in Mehsana District of Gujarat State, India. Karjisan block is a small-sized discovered onshore field with an area of 5 Sq.kms.

The field was discovered by ONGC in 1985. ONGC drilled 1 well for the exploration & exploitation of Kalol pay zones (mainly K-III & IV) and Kadi Formation and discovered gas in pay zone K-III.

The field block was awarded to the Company and a PSC was signed in February 2004 with 100% ownership.

On the basis of updated models, two additional wells KJ-3 and KJ-4 were drilled. In addition to the gas in K-III pay zone, oil was discovered in K- IV payzone in both the wells KJ-3 and KJ-4.

The Estimated Initial Gas in-Place (IGIP) for pay zone K-III: 92 MMscm while the estimated Initial Oil in-Place (IOIP) for pay zone K-IV: 5.81 mn barrels.

As of March 2021, there are 1 out of 2 wells under production in Karjisan Field and daily total production is about 16,000 SCM of gas per day respectively. Gas production and oil production has commenced from KJ-3 and KJ-4.

Other fields

Further, Ministry of Petroleum and Natural Gas (MoPNG) also awarded Contracts for the Ognaj Oilfield to the Company in 2004. The PSC for Indrora field expired on 12 March 2020. The Company had initially applied for an extension of the PSC, however, considering techno–economic reasons, the Company decided not to pursue the said extension.

The Company officially signed the Production Sharing Contract (PSC) extensions for the Bakrol and Lohar PSC’s for a further ten years period ending 2030 with the Government of India after completing all the necessary formalities.

In view of the rapid town planning and urbanization activities in and around Ognaj block area and consequent impossibility to gain access to land as well as high risk to urbanized areas developed around Ognaj block, it had become impossible for the Company to undertake any further operations in the block. Therefore, the Company is left with no choice but to abandon the operations and surrender the block. (Annual Report 2021)

Reserves

Source: Management Presentation 2020

The company has 2P* reserves to the extent of 66.01 Million Barrels of Oil (MMBO) across four fields. Over the years only 4.7% of the entire reserves have been extracted from these fields.

*2P reserves are the total of proven and probable reserves. Proved reserves are likely to be recovered, whereas probable reserves are less likely to be recovered than proved reserves. The sum of proved and probable reserves is represented by 2P.

At the current run extraction rate the Company will generate at least 36,000 barrels of oil and 102,490 MMBTU natural gas per quarter.

Pricing

The Company has assured offtake contracts from the government linked to the market price.

d) Industry

The government of India signed 310 production sharing contracts involving 29 discovered fields (One PSC signed for Panna & Mukta Fields), 28 exploration blocks under pre-NELP Exploration Blocks and 254 blocks under NELP regime with National Oil Companies and Private (both Indian and Foreign)/ Joint Venture companies as licensee /lessee for blocks. Also, 30 Revenue Sharing Contracts (RSCs) have been signed under DSF (Discovered Small Field)-2016 involving 30 Contract Areas. Under HELP (Hydrocarbon Exploration and Licencing Policy), in Open Acreage Licencing Policy (OLAP), Bid Round I, 55 RSCs have been signed on 1st October, 2018. At present out of 310 PSCs & 85 RSCs signed so far under various bidding rounds (Discovered Field, PreNELP, NELP,HELP and DSF), 106 PSCs and 85 RSCs are operational.

Petroleum Exploration Licenses (PEL) for domestic exploration & production of crude oil and natural gas have been granted under different regimes over a period of time:

Nomination Basis: Petroleum Exploration License (PEL) is granted to National Oil Companies viz. Oil and Natural Gas Corporation Ltd (ONGC) and Oil India Ltd. (OIL) on a nomination basis prior to implementation of NELP. Under the Nomination regime, ONGC is operating 9 PEL and 334 PML blocks covering an area of about 94,358 sq. Km. In addition, OIL is operating 3 PEL and 22 PML under the nomination regime covering an area of 5,158 square Kilometres.

Pre-NELP Discovered Field: Petroleum Mining Lease (PML) is granted under small/medium size discovered field Production Sharing Contract (PSCs) from 1991 to 1993 where operators of blocks are private companies and ONGC/OIL has the participating interest. The government of India has signed 28 contracts.

Pre-NELP Exploration Blocks: 28 Exploration Blocks were awarded to private companies between 1990 and prior to the implementation of NELP where ONGC and OIL have the rights for participation in the block after hydrocarbon discoveries.

New Exploration Licensing Policy (NELP) -1999 onwards: Under NELP, exploration blocks were awarded to Indian Private and foreign companies through an international competitive bidding process where National Oil Companies viz, ONGC and OIL also competed on equal footing. The government of India has signed 254 contracts under NELP regime. As on 31st March, 2018, the block under operational are 66 blocks and 188 blocks are relinquished.

Discovered Small Field (DSF) Policy: With a view to increasing domestic production of oil and gas, the Government has brought out the DSF Policy for monetizing the unmonetized/relinquished discoveries of Nomination and PSC regimes. These discoveries clustered in Contract Areas have been awarded under the new regime of the Revenue Sharing Model. To date, two DSF Bid rounds have been conducted. 30 Contract Areas were awarded in DSF Round I and 23 in DSF Round II.

Hydrocarbon Exploration & Production Policy: The government notified Hydrocarbon Exploration and Licensing Policy (HELP) on 30th March 2016 and formally put in operation w.e.f. 1st July, 2017 with notification of Open Acreage Licensing Policy (OALP) and operationalization of National Data Repository (NDR). Under Hydrocarbon Exploration & Licensing Policy (HELP), Government has awarded 94 exploratory blocks on Revenue Sharing basis.

To reduce the import dependency on hydrocarbons & to effectively exploit the untapped established reserves Marginal Field Policy was announced. The policy was later changed to Discovered Small Field Policy (DSF), under the broad policy framework of the new Hydrocarbon Exploration and Licensing Policy (HELP).

“Show me the incentives and I will show you outcome” Charlie Munger

e) Catalyst

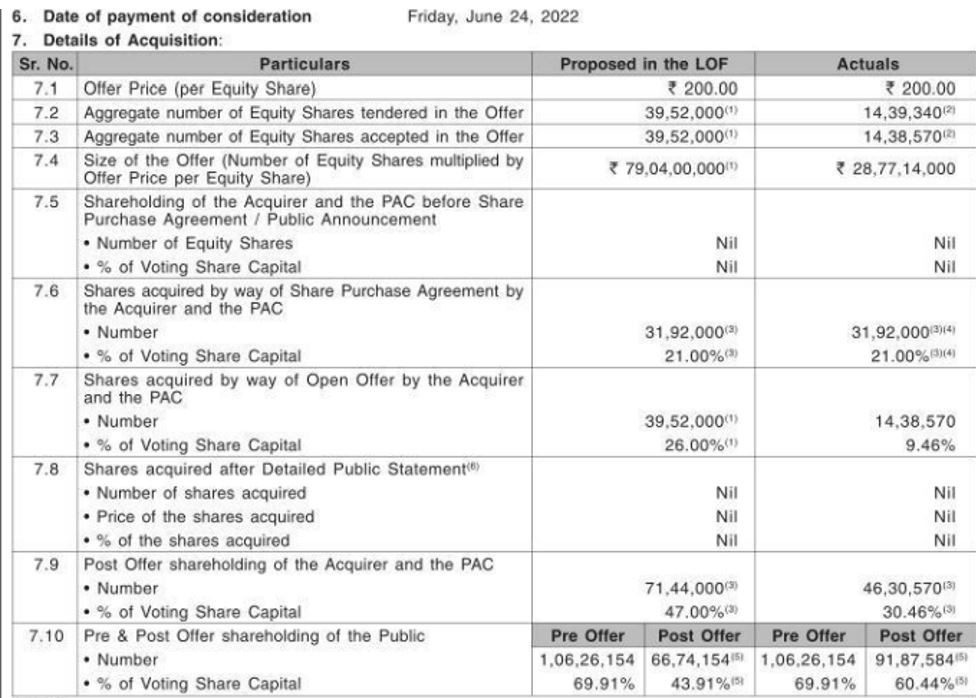

On 17 March 2022 Blackbuck Energy Investment Limited (“BEIL”) entered into share purchase agreement to buy out 21% of the outstanding capital of the Company from the promoters at INR 200 per share (representing c.a. 35% premium to the prevailing market price). This resulted in an open offer through which BEIL made a public offer for an additional 26% stake which recently concluded and BEIL was able to acquire an additional 9.46% in the open offer.

Post the open offer BE now owns 30.46% of the business while the old promoters decided to hang around with c.a. 10% stake in the business.

On July 1st the company updated the exchanges with the latest management and Board changes. Suniti Bhat appointed as the CEO.

So let’s we dive into who is backing BEIL and what story can emerge from this venture.

Antelopus JV Investments PTE (“APIL”) holds majority shares in BEIL (the acquiring entity) while the management team has 25% voting rights in the entity. The management team has preference shares in the entity which probably will convert into equity at some point. APIL is backed by OCM (Oaktree Capital Management) Antelopus Investments Pte (75.19%), Ice Oryx Master Fund (20.05%) and Blackbuck Capital Partners LP (4.76%).

BEIL holds 100% stake in Antelopus Energy Private Limited (“AEPL”) and 30.46% in Selan Oil Exploration. As per the corporate presentation on AEPL’s website they are “an E&P company focused on the Indian Subcontinent.”

“AEPL’s portfolio consists of 2 Contract Areas measuring ~800 Sq. Kms with ~170 mmboe of Discovered Resources in-place.”

The presentation talks about three projects where AEPL has signed deals to extract natural gas and oil in a market-linked mechanism. To know more one can go through their presentation here.

BEIL has been investing in AEPL and as per its last funding around I think the valuation for the business is north of INR 10 bn.

My thesis is that most of the assets in AEPL now need some capex while Selan has a lot of cash but no visible opportunity to deploy this money so at some point there might be a reverse merger between the two entities leading to value unlocking for both. Given the common stakeholder interest that would make a lot of sense.

If you look at the newly appointed Board of Directors at Selan there has been a recent appointment of a legal M&A partner from a reputed firm which suggests that a potential M&A might take place.

f) Unit Economics

Income Statement

I have considered financials over the last three years to get an impression of how the business unit economics have been. For a long time period, one can check out long-range financials on the screener.

This business spends a little over 10% on Operating expenses which are generally fixed since after installing a rig all you have to do is extract oil.

Source: Management Presentation 2020

Per the management, presentation the lifting cost per BOE has been c.a. $25-30. So as more oil is extracted you would have additional revenue flowing through your bottom line.

Although, as oil reserves deplete cost of extraction will increase. So the cost to extract later barrels of oil will be far higher.

Other than the fixed expenses the only large expenses are royalty to the government. It seems that on all oil extracted the company has to pay around 30% of revenues (sharply increased since 2020) to the government as duties.

Management Presentation Mar 2021

The management estimates that over the last decade or so it has generated $226mn while spending $46mn on extracting the oil. The royalty to the government has been $13mn (which is now much higher).

Per my back-of-the-envelope calculation, the company extracts around 100-130k barrels over the last two years (which is half of what it used to do in 2019 and 2020). Although there has been no clarification from the company as to why there was a sharp decline in activity during 2021 there were two major issues:

a) 2020 was a covid year and also the year when oil went negative so it did not make sense to continue production and

b) the company had been finding it difficult to procure a rig (as per some industry sources) in 2019 which led to several delays.

For my 2023 assumptions, I have used a USD/INR 75, Oil price at 90 and production in line with 2022 (although I think it will be much higher with the new management). I think the company will generate cash profits (PAT + Depreciation) of 35-40 crs.

Balance Sheet and Cash Flow

The Company has a fortress of a balance sheet with over INR 200 crores in cash and cash equivalents.

During the current year, the Company generated c.a. 24 crores of CFO (Cash From Operation) less tax after working capital.

The 36 crores transfer to financial assets most likely pertains to the purchase of short-term debt instruments.

Heads, I Win; Tails, I Don't Lose Much. Mohnish Pabrai

g) Valuation

Looking at valuation from a few metrics:

i) Given the fixed nature of contracts (ie 10 years), one could use a dcf and plug-in yearly extraction rate and run a model. Since I do not have a lot of data around it I use a reverse dcf and figure out what are market expectations.

ii) The current EV of the business is c.a. 60 crores and the business would generate an EBIT of c.a. 23 crores and cashflows of around 35 crores (add back tax adjusted amortization to EBIT) next year. So this business will return your capital in 3 years or basically the market discounts this business at 33% (just flipping the ratios).

My thesis rests more on the micro side how management executes over the next two to three years. I am still reading on the dynamics of Oil industry which has always eluded me given the dynamic and wide range of outcomes in the industry. I am waiting for the management to come out with a strategic business direction. At the moment I have a tracking position.

I cannot advise on buy/sell decision or portfolio allocation but my experience is that a typical turnaround is a multi year journey with possible negative surprises (there always is) so price might do nothing for a while. So position sizing should be assessed accordingly.

Hope that helps.

Excellent.

I liked it very much.

Keep going sir......